Wednesday, December 11, 2013

A different approach

I have discovered a different investment vehicle from typical trading which seems to suit a trading style that I am working on. They are called binary options, and I am working on improving an already working (so far) stradegy for trading 60 second binary options. You can follow my progress at tradertuition.com

Thursday, May 6, 2010

Someone tripped over the power cord

What an unreal unraveling of the market today! The SPY was dropping off a cliff, caused by PG company stock puking its guts out, from a hedge fund short circuit, dogs and cats- living together, mass hysteria! I was shaking my head the rest of the day. Just wow.

Here's what CNBC are calling the culprit:

According to multiple sources, a trader entered a "b" for billion instead of an "m" for million in a trade possibly involving Procter & GambleIt goes on to say "the erroneous trade may have been made at Citigroup"...I wonder how much losses resulted in this mistake? A sell market order for over a billion shares? It made over a 20 point move during the sell off...I would hate to be that guy.

I wonder if that is an accurate tick, that almost is too hard to believe if it is.

The SPY was ripped open as well, the big elevator shaft in the middle of the chart, followed with an incredible price swing from off the bottom. The resulting move took the SPY back 9.3 points (in 3 minutes 33 seconds!)

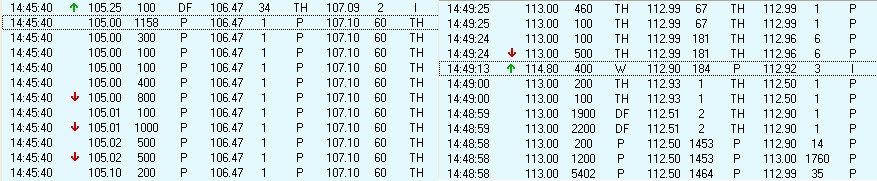

Time and sales of the tops and bottoms

Just unreal

As far as my savings go - I will have a pretty good May (even with having the decent expenditure to get some car repairs for state inspections) which is great since I will be able to execute on my plan to consolidate my debt into my 401k faster. Now to stay on track I next need to set up a budget...more to follow with that.

Sunday, April 25, 2010

Fine tuning

I think my initial proposal was a good one, and it lays some pretty good groundwork for getting my debt paid down smoothly and quickly. I was thinking about the most economical way of paying down my debt would need a bit more fine tweaking.

My largest concern is the high interest rate on my credit card, I will need to verify the % APR, but my card was one of the thousands that the credit card company sent out a letter saying they were about to raise rates, and I could cancel the card altogether if I didn't agree to the terms. No one to blame here but myself for the account balance, but I felt a bit dirty when that happened, and now I am paying somewhere in the ballpark of 20%.

Now I don't have a bond calculator to make this into an exact calculation of interest paid, but a $7,500 account balance at that rate is about $125 per month in interest alone. That's actually more than my car insurance and my cell phone bill together.

What I will do to change my strategy is to pay off my small 401k loan first, which could be done in about 2 months at the rate of savings I am shooting for. Then I would look to take out a bridge 401k loan (I can have a max of 2 out at a time) to pay off my credit card completely. This way I would no longer carry a credit card balance in about 2 months time, I would then be set to handle my accounting by funneling all expenses through the credit card asap, and lastly save myself some cash in interest. However the downside is I would significantly reduce my 401k balance for the time being. While I do not see much upside to the market in the next few months and if it does drop, I can average back in at a lower price in my 401k...but a big missed opportunity if the market does continue to climb.

This move should save me a few hundred dollars in credit card interest, and also convert all the debt into very low interest loans, setting me up for an easier payoff time.

My largest concern is the high interest rate on my credit card, I will need to verify the % APR, but my card was one of the thousands that the credit card company sent out a letter saying they were about to raise rates, and I could cancel the card altogether if I didn't agree to the terms. No one to blame here but myself for the account balance, but I felt a bit dirty when that happened, and now I am paying somewhere in the ballpark of 20%.

Now I don't have a bond calculator to make this into an exact calculation of interest paid, but a $7,500 account balance at that rate is about $125 per month in interest alone. That's actually more than my car insurance and my cell phone bill together.

What I will do to change my strategy is to pay off my small 401k loan first, which could be done in about 2 months at the rate of savings I am shooting for. Then I would look to take out a bridge 401k loan (I can have a max of 2 out at a time) to pay off my credit card completely. This way I would no longer carry a credit card balance in about 2 months time, I would then be set to handle my accounting by funneling all expenses through the credit card asap, and lastly save myself some cash in interest. However the downside is I would significantly reduce my 401k balance for the time being. While I do not see much upside to the market in the next few months and if it does drop, I can average back in at a lower price in my 401k...but a big missed opportunity if the market does continue to climb.

This move should save me a few hundred dollars in credit card interest, and also convert all the debt into very low interest loans, setting me up for an easier payoff time.

Subscribe to:

Comments (Atom)